One of the (many) things my wife regularly jabs me about is the fact that I refuse to (or give the appearing of refusing to) daydream about money. What this means, in other words, is that I don't spend much time answering the question, "What would you do if you won the lottery?"

Every so often she'll ask me that. It's just for fun, because I could probably count on one hand the number of Lotto tickets I've purchased in my lifetime. I don't get anything out of playing the lottery, to be honest. I've been to Las Vegas, and I didn't get much out of that, either. If I'm gonna blow a dollar or five somewhere, it'll be for something I really like and/or value: Maybe a Cherry Coke, or a new Dr. Grip pen, or a used book of some sort. Stuff like that.

Here's the thing: If I won a multimillion-dollar lottery, I wouldn't do anything ridiculously creative. I'm boring by nature, and as Dave Ramsey says, "More money just makes you more of what you already are." I mean, I'd probably do what a fair amount of other folks would do. I'd keep going to work for a while. I wouldn't stop going to work until I could a feel for the New Big Money. Once that happened, though, I might just bide my time until that one special Pain In the Ass customer came through. At that point, I'd unload a few years' worth of frustration on them, clue them in to How the World Really Works, and then I'd pack my stuff and be out the door. Thanks for playing. It's been real.

But last night Lisa (my wife, for those new to the show) asked a more interesting question: What would you do if you won (after taxes) only $2,000? What if you won $10,000? How about $50,000?

Those sums aren't astronomical, to be sure. Some discretion and forethought would be required (if you're someone who understands the nature of money and wealth, anyway) in order to maximize the benefits of your Moderate Good Luck. Yes, when you when millions, you still have to avoid American Dumbass Syndrome and pay attention to your money, or else it will just go away. But when your winnings aren't up to that handful-of-millions mark, the spending and/or saving decisions are quite a bit different. You kind of have to focus.

If I Won Some Money...

Okay, here goes the daydreaming.

If I Won $2,000: I'd use it for repair/remodel of our house. If I Won $10,000: See above. If I Won $50,000: Pay off our Honda. Then repair/remodel our house. Then save the rest. Okay ... I might buy a big HDTV and new entertainment center. Might.

What Would You Do?

How would you make sure you were actually financially better off after winning your 2 or 10 or 50 thousand bucks? Or would you do the patriotic, Joe Sixpack thing, and blow it all on 20-inch rims or a sweet new ride that the guys 'n' chicks seriously dig?

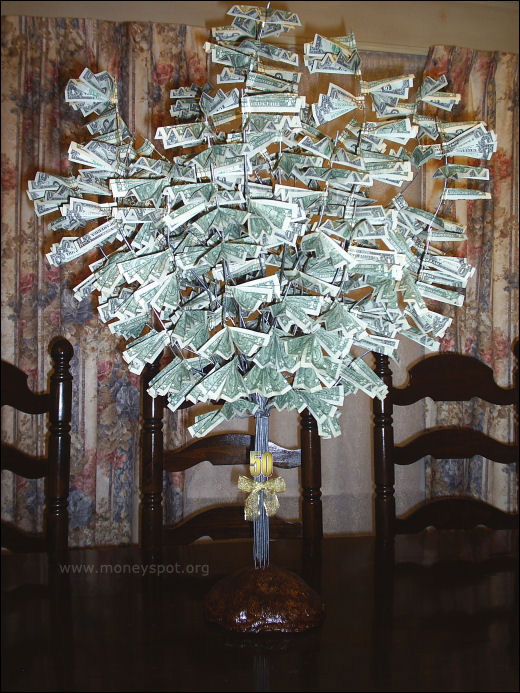

I've never actually seen a Money Tree in real life, I don't think. But I think it's a totally cool idea.

The Money Tree pictured here (click to see a larger version) was created by ExcelGeek, the guy behind the World's Best Freedom Account spreadsheet, which I happily offer on my main site.

Of course I asked him how he built the thing. For anyone interested in such details, this was his response:

I used common suspended-ceiling wire (cheap), cut into odd lengths; gathering the wire together with a couple of hose clamps and bent it into a tree-like shape. The base end is flared and planted (like rebar) into a "glob" (highly technical term) of plaster of paris, which I stained brown to look like dirt and sealed it with about 10 coats of polyurethane. The whole thing stands about 3-1/2 feet tall and is very solid.

ExcelGeek built the Money Tree as a gift for his parents on their 50th Wedding Anniversary. Congrats, Mom and Dad ExcelGeek! Now you know what your son does in his spare time!

Getting (and keeping) a grip on your finances isn't an easy task. Every so often (like yesterday) a frazzled reader will ask, "How do you do it?"

Well, I'll tell you. My system works like this:

The Grand Overview

I track all accounts, balances, and financial transactions in Quicken 2006 Premier Home & Small Business. This is also where I categorize my past and current spending, as well as monitor my net worth, assets and liabilities, and investments. I also use it to track all my small-business (namingly, this website and my wife's jewelry/craft business) inflows, outflows, and accounts. Quicken is also a tremendous tool for handling all tax-related items and accounts. I use the heck out of it for this. Is Quicken pricey? Yes, the fancier versions can be. Does it require a fair bit of learning time? Yes, though this also depends on what version you get and what you want to use it for. Would I give it up? No way. Not a chance.

Monthly Spending Plan / Budget

For all that I love about Quicken, I absolutely despise its budgeting setup. It's cluttered, nonsensical, and useless to me. So, to budget (as well as monitor in real time) my spending for each month, I use a slightly-modified version of my Excel Spending Plan (v2.0). You can download it from the near-bottom of my Excel financial spreadsheets page. And more details can be found at my Spending Plan page.

Emergency Fund

I don't have a specific spreadsheet that I use to track my Emergency Fund. However, I do keep most of my E-fund (say, 90% of it) in its own account at Emigrant Direct (review). Any transactions that affect my Emergency Fund get logged/tracked in Quicken, as noted above, and I can always see its balance right there in my Quicken toolbar.

Freedom Account

I use ExcelGeek's Freedom Account spreadsheet to track my Freedom Account and all its subaccounts and balances. I keep my Freedom Account funds at ING DIRECT (review), in an account that's separate from everything else. If you've never heard of Freedom Accounts before, or if you're just not sure what exactly they can do for you, head over and check out my Freedom Account page.

What combination of software (and/or notebook paper!) do you use?

Anybody else seen this Century 21 commercial lately?

That ad makes me shudder. Can't you just feel that couple burying themselves in a mortgage they have NO business taking on? How about that look (contempt? disbelief?) on the wife's face at 00:14 in the clip? Impressive.

Here's the question that runs through my mind: "Okay, Suzanne. What happens when the zero-down, stated-income ARM resets, our kids are older and even more expensive, and the cars we had earlier weren't 'nice' enough to fit in that huge garage, so we upgraded those, too? What then?"

It does take on a whole new (amusing) meaning when you follow it up with this one:

The Fatwalleters are in dismay again: Emigrant Direct has dropped its savings rate from 5.15 APY to 5.05 APY.

Emigrant had been a rate leader, or very close to it, since July 28 or so. That's when they last lifted their American Dream savings account rate. Now, its current APY of 5.05 puts it in a still-admirable group of other online savings institutions that pay rates at 5% or better (HSBC, GMAC, and a host of others).

As I opined in my Emigrant Direct review, there are a host of reasons to like Emigrant (very fast ACH transfers, multiple linked accounts, etc.), and this rate change doesn't affect that. Interest-rate fluctuations, both to the up- and downsides, are a natural part of banking and economic life. Rate changes, as the bumper sticker would say, happen.

The issue at heart here (for most money bloggers, anyway) is one of whether old rate leaders ever return to rate greatness. Witness what's happened to ING Direct (review): They were the standalone rate leader at one time. Then they got big and popular . . . and were able to rest on their laurels . . . and now their rates are firmly at the back of the online-savings pack. There are still good reasons to have an ING Direct account. Interest rates, however, aren't one of them.

Now, if you're a devout rate-chaser, then it may indeed be time to start looking elsewhere. Actually, if you're really devout, you probably already have ... and your money is on its way to E-LOAN.

E-LOAN is the newest player in the online-savings game — and as is common for such new entrants, they're offering a rate (5.5 APY) that tops most everyone else. They also require a $5,000 minimum opening deposit, though, and can be linked to only one outside account. So at least for now, they're not for everyone.